Accounting for SPAC Warrants

Background

As part of SPAC‘s formation, the newly formed company issues its founders or sponsors shares in exchange for nominal amount of equity capital. Sponsors may also provide the SPAC with debt financing. Debt and equity capital are used to fund entity’s formation and the cost of the initial IPO.

As part of the IPO, SPACs issue its founders warrants, i.e., equity-linked instruments that give SPAC’s founders an option to buy additional shares of the entity in the future at the price agreed in the warrant agreement. The warrants issued to sponsors are referred to as “private”. Warrants are also issued to public investors in connection with their purchase of SPAC’s IPO shares. Terms of private and public warrants have certain differences. Main differences concern rights of warrant holder to transfer the warrant and issuer’s cash redemption rights.

Generally, both types of warrants have the same exercise price and the term. Warrants can only be exercisable 30 days after completion of SPAC merger but not earlier than 12 months after SPAC initial IPO. The exercise price is subject to certain adjustments as described in the warrant agreement.

The question is how to classify and measure warrants issued by SPACs in accordance with US GAAP and SEC accounting guidance. Historically, many SPACs classified private and public warrants as equity instruments.

On April 12, 2021 SEC has issued a public statement on Accounting and Reporting Considerations for Warrants Issued by SPACs. In the statement SEC has described certain warrant terms that would be inconsistent with equity classification. SEC has noted warrant settlement provisions where all warrant holders would be entitled to receive cash for their warrants upon successful completion of a merger with an operating company. While all warrant holders will be entitled to cash, only certain holders of common stock would be entitled to cash. Given the disparity in treatment of equity and warrant holders, SEC has concluded the above warrants should be classified as a liability instrument.

In the public statement SEC staff has also noted that the above potential cash payment to warrant holders represents a settlement provision that would not be consistent with inputs used to determine the fair value of a fixed-for-fixed equity option.

SEC has indicated that the warrants in question should be classified as liabilities, not equity.

Executive Summary

Public and private warrants are considered freestanding financial instruments. Many SPACs have concluded that the warrants are not in the scope of ASC 480.

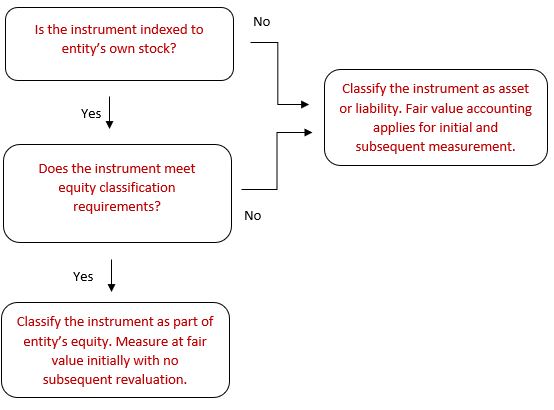

Detachable warrants are classified as an equity instrument if the instrument is indexed to entity’s own stock and meets other equity classification requirements. If any of the above equity classification requirements are not met, the instrument is considered a liability. In this case, it is measured at fair value initially and subsequently. Changes in the fair value are reported in the income statement.

Indexation guidance has two steps. Step one focused on exercise contingencies while step two deals with settlement provisions, i.e., potential adjustments to the exercise price or the amount of issuable shares. As part of step two analysis, settlement provisions will not preclude equity classification if the exchange terms are as such that fixed number of entity’s shares is exchanged for fixed monetary amount, i.e., fixed exercise price, subject to certain exceptions. The above rule is referred to as “fixed-for-fixed”. Certain other adjustments comply with step two requirements including adjustments based on inputs to the valuation model used to determine the fair value of a fixed-for-fixed forward or option on equity shares.

If an entity is required to settle an equity-linked instrument in cash due to the occurrence of fundamental transaction (i.e. change of control), the instrument has to be classified as a liability unless, according to the terms of fundamental transaction, all holders of underlying shares are entitled to cash. Existing standard terms of warrants issued by SPACs contain certain adjustments to the exercise price and warrant redemption value in the event of fundamental transaction. Specifically:

- In the event of fundamental transaction, as defined in the agreement, warrant holders can be entitled to more favorable settlement that some shareholders will be;

- In the event of fundamental transaction, as defined in the agreement, private and public warrant holders can be entitled to a different settlement amounts;

- Definition of fundamental transaction in standard terms is inconsistent with U.S. GAAP definition of the change of control.

Each of the above terms, individually trigger classification of both private and public warrants as liability instruments.

Cash redemption terms applicable to public warrants, cashless settlement terms of private warrants and SPAC’s net share settlement of both warrants triggered by the trading of shares at least $ 10 per share prevent equity classification of both types of warrants. Specifically:

- Different settlement terms including cash redemption of public warrants and cashless exercise of private warrants prevent private warrants from being classified as equity instruments;

- Existing warrant table specifying the number of net issuable shares depending on remaining terms and stock trading value prevents equity classification of both private and public warrants;

Consistent with SEC observations, existing standard terms of public and private warrants issued by SPACs prevent their classification as equity instruments.

In an effort to establish warrant terms consistent with equity classification requirements, many SPACs made the following changes to the warrant agreement: a) removed or substantially modified terms of fundamental transaction; b) aligned terms of public and private warrants; c) removed or substantially modified the warrant table.

SPAC sponsors and their service providers may consider alternative warrant terms, which will require balancing commercial interests of SPAC public investors, SPAC management and the sponsor.

Equity-Linked Financial Instruments: Accounting Guidance

A warrant is a written call option represents a type of an equity-linked instrument. U.S. GAAP guidance covering equity-linked instruments is provided in ASC 815, Derivatives and Hedging.

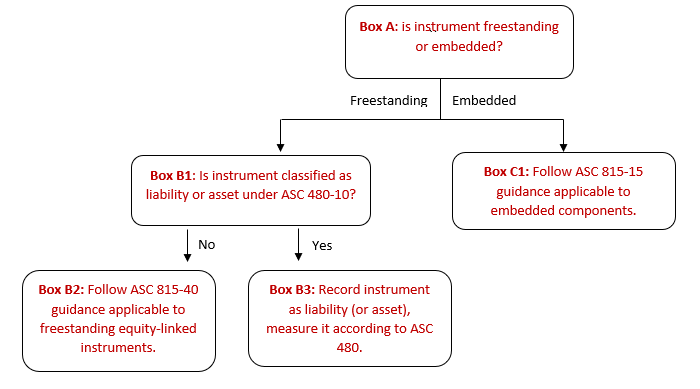

Appendix A: Accounting for Equity-Linked Instruments shows an overall approach to accounting for warrants and other equity-linked financial instruments. Appendix B: Accounting for Freestanding Equity-Linked Instruments shows an overall approach to accounting for detachable warrants and other freestanding equity-linked financial instruments. The analysis in Appendix B does not apply to warrants that are not considered detachable, i.e. freestanding instruments.

Box A Freestanding vs. Embedded: Current accounting guidance has different set of rules applicable to so embedded and freestanding instruments. An instrument is considered freestanding if either of the following two conditions apply:

- the instrument is entered into separately and apart from any of the entity’s other financial instruments;

- it is entered into in conjunction with some other transaction and is legally detachable and separately exercisable;

“Legally detachable” generally refers to ability of the instrument holder to legal transfer, e.g., sale the instrument without transferring all other related instruments, e.g., equity shares originally issued along with warrants.

Public warrants can be “detached” from the shares they were originally issued with and transferred to a different holder through a market mechanism subject to 52-day time window as described in par. 2.5 of the standard warrant agreement. Generally, public warrants are considered freestanding instruments.

Private warrants will be transferrable by their original holders only subsequent to Company’s initial business combination transaction. However, private warrants were issued as separate financial instruments to sponsors in connection with the IPO. According to an extract from ASC 815-15-25-2:

The notion of an embedded derivative in a hybrid instrument refers to provisions incorporate into a single contract, and not to provisions in separate contracts between different counterparties….

Since private warrants were sold as part of a separate contract between SPAC and the sponsor, the warrants are considered freestanding instruments.

Overall, warrants issued by SPACs likely represent freestanding instruments.

Box B1 Scope of ASC 480: Next step in the analysis is to determine if the instrument is included in scope of ASC 480, Distinguishing Liabilities from Equity. ASC 480 applies to freestanding equity-linked instruments considered mandatorily redeemable or meeting other specific requirements. Generally, instruments included in the scope of ASC 480 are considered liability (or asset) instruments.

Mandatorily redeemable shares are defined as instruments that embody an unconditional obligation requiring the issuer to redeem the instrument, at the option of the holder, by transferring its assets at a specified event or upon an event that is certain to occur (ASC 480-10-20, Glossary). When the obligation is conditional, e.g., it depends on an uncertain event, the instrument becomes mandatorily redeemable if the event occurs or becomes certain to occur (ASC 480-10-25-5). Redemption linked to entity’s liquidation or dissolution does not trigger liability classification (ASC 480-10-25-4).

Redemption of SPAC Shares: SPAC public shareholders may, at their option, redeem ordinary shares upon completion of business combination transaction subject to certain limitations. According to SPAC certificate of incorporation, the entity will not redeem its public shares in an amount that would cause SPAC net tangible assets (NTA) to be less than $5,000,001. Generally, redemption of shares in connection with the merger applies to public but not private shares. SPAC will redeem public if no business combination transaction takes place. Generally, the aggregate redemption value is the amount held in the trust account at the time of the redemption including interest less related taxes. Terms of liquidation redemption also apply to shares held by the sponsor acquired after the initial IPO.

Additionally, many SPACs restrict the amount of redemption by a single shareholder (or affiliated group) 20% of total public shares in the event management seek shareholder approval of the merger and does not conduct redemptions pursuant to the tender offer. The decision to seek shareholder approval of a proposed business combination or conduct a tender offer will be made by the Company at its discretion unless the terms of the transaction would require the Company to seek shareholder approval under the law or stock exchange listing requirements.

A share redeemable at the option of the issuer or the holder, or share redemption contingent on the occurrence of an uncertain event, does not meet the definition of a mandatorily redeemable instrument before the option is exercised or the event occurs. The above view is based on par. B25 of the Background Information and Basis for Conclusions of FASB Statement 150:

Board considered whether to include within the scope of this Statement shares that could be redeemed – mandatorily, at the option of the holder, or upon some contingent event that is outside the control of the issuer and the holder. However, this Statement limits the meaning of mandatorily redeemable to unconditional obligations to redeem the instrument by transferring assets at a specified or determinable date (or dates) or upon an event certain to occur.

Since ordinary public shares are redeemable at the option of the holder and upon occurrence of the merger or, mandatorily, in the event of liquidation (i.e. if no merger occurs), the shares are not considered mandatorily redeemable, from the ASC 480 perspective.

Management noted that warrants issued on contingently redeemable (puttable) stock may still be considered a redeemable instrument subject to ASC 480. According to ASC 480-10-55-33:

A warrant for puttable shares conditionally obligates the issuer to ultimately transfer assets—the obligation is conditioned on the warrant’s being exercised and the shares obtained by the warrant being put back to the issuer for cash or other assets. Similarly, a warrant for mandatorily redeemable shares also conditionally obligates the issuer to ultimately transfer assets—the obligation is conditioned only on the warrant’s being exercised because the shares will be redeemed. Thus, warrants for both puttable and mandatorily redeemable shares are analyzed the same way and are liabilities under paragraphs 480-10-25-8 through 25-12, even though the number of conditions leading up to the possible transfer of assets differs for those warrants. The warrants are liabilities even if the share repurchase feature is conditional on a defined contingency.

The above requirements cover warrants on shares that may require transfer of assets, i.e. conditional obligations, not just mandatorily redeemable shares.

A warrant on a redeemable preferred share that may require the issuer to transfer assets is a liability unless the issuer can avoid triggering redemption by controlling the exercise contingency. If the future event that triggers the redemption (or possible redemption) of the preferred shares is completely within the issuer’s control, an obligation does not exist and will not exist until the issuer takes (or fails to take) action. Accordingly, the share is not considered redeemable. An argument can be made that SPAC’s management controls initiation of the merger and, therefore, can prevent redemption in connection with the merger transaction. If so, the warrants will not be considered in the scope of ASC 480.

As noted above, the warrants become exercisable 30 days after completion of business combination but not earlier than 12 months after SPAC’s IPO (par. 3.2 of standard warrant agreement). At that point, ordinary shares will not be redeemable. Since, no redeemable shares can be issued upon exercise of the warrant, shares underlying the warrant are not considered contingently redeemable.

Based on the above considerations, many SPACs have concluded that private and public warrants are not subject to ASC 480.

The above analysis covers redemption features associated with the underlying shares. Redemption of the warrant as a freestanding instrument is analyzed in a separate section of this paper.

Generally, SPAC warrants do not meet requirements for other types of instruments described in ASC 480-10-25-14 and included in the scope of ASC 480.

Box B4: Indexation Guidance The analysis starts with the question of whether the instrument is indexed to entity’s own stock. Generally speaking, instruments are indexed to entity’s own stock when economic characteristics and risk of the instrument are similar to those of entity’s equity.

The so-called indexation guidance requires an entity to apply a two-step approach (ASC 815-40-15-7). Step 1 covers the evaluation of instrument’s contingent exercise provisions, if there are any. Step 2 is focused on the analysis of instrument’s settlement provisions.

An exercise contingency shall not preclude an instrument from being considered indexed to an entity’s own stock provided that it is not based on either of the following:

- An observable market, other than the market for the issuer’s stock (if applicable)

- An observable index, other than an index calculated or measured solely by reference to the issuer’s own operations (for example, sales revenue of the issuer; earnings before interest, taxes, depreciation, and amortization of the issuer; net income of the issuer; or total equity of the issuer).

The warrants can only be exercised subsequent to completion of a merger transaction (par. 3.1 of the standard warrant agreement). An exercise condition linked to the change in control or merger involving the reporting entity is not based on an observable market or index. Therefore, such a settlement condition does not prevent equity classification.

As part of Step 2, management should evaluate all adjustments to instrument’s exercise price as well as the amount of issuable shares. Generally, settlement provisions will not preclude equity classification if the exchange terms are as such that fixed number of entity’s shares is exchanged for fixed monetary amount, i.e., fixed exercise price, subject to certain exceptions. The above rule is referred to as “fixed-for-fixed”. In a way, Step 2 requirement draws an analogy to general terms applicable to issuance and sale of equity, e.g. common stock when fixed amount of shares is exchanged for fixed consideration.

Certain other adjustments comply with Step 2 requirements. Such adjustments include:

- variables used as inputs to the valuation model utilized to determine the fair value of a fixed-for-fixed forward or option on equity shares (ASC 815-40-15-7E);

- equity restructuring adjustments including stock dividend, stock split, spin-off, rights offering or recapitalization through a large, nonrecurring cash dividend (ASC 815-40-20, Glossary);

- down round protection clauses (ASC 2017-11);

- subjective modification provisions benefiting the counterparty, not the reporting entity (ASC 814-40-15-7H);

- terms of fundamental transactions triggering payment to debt holders of the same consideration (e.g., cash, debt, etc.) that will be provided to all stockholders impacted by the transaction (ASC 815-40-55-2 through 55-6);

In this paper we cover settlement adjustments specifically relevant to standard terms of SPAC warrants, i.e. items 1. and 5.

Generally, if the entity may be required to settle the warrant in cash, the warrant is considered a liability instrument. According to ASC 815-40-25-7:

Contracts that include any provision that could require net cash settlement cannot be accounted for as equity of the entity (that is, asset or liability classification is required for those contracts), except in those limited circumstances in which holders of the underlying shares also would receive cash.

Cash settlement prevents equity classification regardless of the probability of the settlement event or scenario. However, certain other provisions in the US GAAP imply that if net cash settlement can be triggered only by the event that is solely within the entity’s control, such a net cash settlement provision does not preclude equity classification. The above treatment is based, in part, on ASC 815-40-25-8:

Generally, if an event that is not within the entity’s control could require net cash settlement, then the contract shall be classified as an asset or a liability. However, if the net cash settlement requirement can only be triggered in circumstances in which the holders of the shares underlying the contract also would receive cash, equity classification is not precluded.

Inputs in Pricing of Fixed-For-Fixed Instruments

If a potential adjustment to the settlement terms is consistent with the inputs used in the valuation of a fixed-for-fixed option (e.g., stock price, exercise price), the instrument is considered indexed to the entity’s own stock. Examples of qualifying inputs include risk-free rates, stock volatility, expected dividends, entity’s credit spread and term/duration of the instrument. However, in situations when a contract contains a settlement feature that results in greater exposure to an input or a variable than the exposure to the input in the pricing of a fixed-for-fixed option, the contract is not considered indexed to entity’s own stock. Similarly, if the settlement amount varies in response to changes in inputs other than those used in the fair value measurement of a fixed-for-fixed equity option, the instrument is not indexed to the reporting entity’s stock. Ineligible variables include entity’s operating metrics e.g., revenue, EBITDA, etc., inflation rate, commodity prices, etc.

To illustrate the above point, if the terms of the warrant provide for the increase in the amount of issuable shares if entity’s revenue in a given fiscal year increases by more than 10% from the prior year, such an adjustment will be considered inconsistent with equity classification. This is because entity’s revenue is not an input in the standard Black-Scholes valuation model.

Fundamental Transaction

Many warrants contain special provisions impacting settlement terms in the event of a fundamental transaction. The term fundamental transaction is defined to include a sale of substantially all of company’s assets, change in control through a merger or otherwise and other similar transactions. Certain fundamental transactions are executed through a tender offer, i.e. a public offer to purchase some or all of shareholders’ shares.

In the event of a fundamental transaction, terms of some warrants state that warrant holders can be entitled to cash payable in exchange for their warrants. For example, warrant terms may specify that warrant holder shall have the right to receive, for each warrant share that would have been issuable upon exercise immediately prior to the occurrence of a fundamental transaction, at the option of the holder the number of shares of common stock of the successor company or any other consideration (“alternate consideration”) receivable as a result of such fundamental transaction by a holder of common stock.

As noted above, warrants that an issuing entity could be required to settle in cash should be accounted for as a liability. However, implementation guidance in ASC 815-40-55-2 through 55-5 specifically discusses circumstances where equity classification is appropriate despite the possibility of a cash settlement if holders of the same class of underlying shares also would receive cash in exchange for their shares:

55-2 An event that causes a change in control of an entity is not within the entity’s control and, therefore, if a contract requires net cash settlement upon a change in control, the contract generally must be classified as an asset or a liability.

55-3 However, if a change-in-control provision requires that the counterparty receive, or permits the counterparty to deliver upon settlement, the same form of consideration (for example, cash, debt, or other assets) as holders of the shares underlying the contract, permanent equity classification would not be precluded as a result of the change-in-control provision. In that circumstance, if the holders of the shares underlying the contract were to receive cash in the transaction causing the change in control, the counterparty to the contract could also receive cash based on the value of its position under cone contract.

55-4 If, instead of cash, holders of the shares underlying the contract receive other forms of consideration (for example, debt), the counterparty also must receive debt (cash in an amount equal to the fair value of the debt would not be considered the same form of consideration as debt)

55-5 Similarly, a change-in-control provision could specify that if all stockholders receive stock of an acquiring entity upon a change in control, the contract will be indexed to the shares of the purchaser (or issuer in a business combination accounted for as a pooling of interests) specified in the business combination agreement, without affecting classification of the contract.

The nature of the above provisions is that if warrant holders have the same economic position in a fundamental transaction as other equity holders do, cash payment to the warrant holders do not preclude equity classification. Generally, for the warrant to be eligible for equity classification, the terms of fundamental transaction should specify that warrant holders will receive the same form of consideration as all holders of the underlying shares do.

As noted above, FASB’s view is that a change of control transaction is outside of entity’s control. The above view is based on the presumption that entity’s management may not be in a position to prevent fundamental transaction which takes place, for example, as a result of hostile take-over or shareholder vote.

Box B6: Additional Equity Classification Requirements If the warrants are considered indexed to entity’s own stock, the next step in the analysis is to consider additional equity classification requirements. Generally, additional equity classification requirements are intended to identify situations when the warrant holder can force the issuer to settle the instrument in cash and not in equity.

The additional equity classification requirements as stated in ASC 815-40-25-10 are as follows:

- Settlement is permitted in unregistered shares;

- Entity has sufficient authorized and unissued shares;

- Contract should contain an explicit limit on the number of shares to be delivered;

- No required cash payment if entity fails to make timely filings with SEC;

- No cash-settled top-off or make-whole provisions;

- No counterparty rights rank higher than shareholder rights;

- No collateral required;

Recently issued ASU 2020-06 eliminated requirements 1, 6 and 7 above. The new guidance is effective for SEC filers, excluding smaller reporting companies, for fiscal years beginning after December 15, 2021. For all other entities, the amendments are effective for fiscal years beginning after December 15, 2023. Early adoption is permitted, but no earlier than fiscal years beginning after December 15, 2020.

Whether the entity has sufficient authorized and unissued shares is determined considering other agreements that may obligate SPAC to issue common stock, e.g. forward equity agreements. We understand that, in general, the amount of authorized common shares at the time of the IPO is determined as such that SPACs have enough unissued shares to satisfy their obligations under the terms of agreements involving issuance of SPAC shares.

Additional equity classification requirements should be carefully analyzed to determine if the entity meets them.

Instruments that meet all equity classification requirements are considered equity. Otherwise, the instrument has to be classified as an asset or liability. In this case, the instrument will be measured at fair value initially and subsequently with remeasurement adjustments reported in entity’s income statement.

Analysis of SPAC Standard Warrant Terms

Many SPACs use a warrant agreement with standard terms covering public and private warrants. Standard terms describe the impact of fundamental transaction, redemption, transfer and other relevant rights and obligations. Standard terms also clarify conditions and amount of certain adjustments to the exercise price and the amount of issuable shares.

Terms of Fundamental Transaction/Tender Offer

Appendix C: Terms of Fundamental Transaction and Accounting Considerations provides analysis of standard terms of fundamental transaction and relevant accounting considerations. The above terms are presented in par. 4.6 of the standard warrant agreement.

Based on the information provided in par. 4.6 as analyzed in the appendix:

- In the event of fundamental transaction, as defined in the agreement, warrant holders may be entitled to more favorable settlement that some shareholders will be;

- In the event of fundamental transaction, as defined in the agreement, private and public warrant holders can be entitled to a different settlement amounts;

- Definition of fundamental transaction in standard terms is inconsistent with U.S. GAAP definition of the change of control.

Any of the above consideration individually would prevent classification of both public and private warrants as equity instruments.

SPAC Standard Warrant Terms: Entity’s Redemption, Cashless Exercise

A SPAC may, at its own discretion, to redeem public warrants when they become exercisable and provided certain conditions are met. Specifically, SPAC may redeem public warrants while they are exercisable at $ 0.01 per warrant, when the market price of SPAC’s shares reaches $18.00 (par. 6.1 of the standard warrant agreement). Stock redemption is performed by issuing a 30-day redemption notice. The above cash redemption terms do not cover private warrants.

Redemption of public warrants is at SPAC option and is within its control. Therefore, as such, the above cash redemption terms do not prevent classification of public or private warrants as equity instruments.

Private warrants can also be exercised at any time during the exercise period on a cashless basis, at the option of the holder. Public warrants do not have the same exercise option.

When private warrants are transferred to certain non-permitted transferees, private warrants will inherit characteristics of public warrants.

Under the above provisions, warrants settlement value depends on the characteristics of the warrant holder. Since such characteristics are not considered inputs in the fair value of a fixed-for-fixed equity forward or option, the above settlement terms would be inconsistent with equity classification requirement. We understand that SPAC’s cash redemption and cashless settlement terms are interpreted as settlement characteristics specifically attributable to private warrants. Therefore, the above terms prevent equity classification of private but not public warrants.

SPAC warrant agreements also contain provisions which permit the issuer to force the exercise of public and private warrants on a net share basis, if the stock market price equals or exceeds $10.00. In this case, the number of issuable shares is determined by reference to a table (“warrant table”) and varies based on the then-current stock price and remaining warrant term. We understand that settlement amounts in the warrant table were determined using standard Black-Scholes model with an expected volatility being higher than the volatility number that would have been determined at the time the warrant agreement was executed. Use of overstated volatility as an input to determine the settlement amount is inconsistent with determining fair value of a fixed-for-fixed equity forward or option. Therefore, the above settlement terms would prevent equity classification of both private and public warrants.

Based on the analysis of cash redemption and net share settlement terms:

- Different settlement terms including cash redemption of public warrants triggered by $ 18 stock price and cashless exercise of private warrants prevent private warrants from being classified as equity instruments;

- Existing warrant table specifying the net number of issuable shares depending on remaining terms and stock trading value prevents equity classification of both private and public warrants;

Consistent with SEC observations, existing standard terms of public and private warrants issued by SPACs prevent their classification as equity instruments.

Reassessment Requirements

The reporting entity should reassess equity vs. liability classification at the end of each reporting period (ASC 815-40-35-8 through 35-10). Equity classified warrants may have to be re-classified as a liability and vice versa. Reclassification is often times triggered by changes in relevant facts and circumstances including assessment of meeting additional equity classification requirements in ASC 815-40-25-10 or warrant terms.

If a warrant previously classified as equity no longer meets equity classification requirements, it has to be re-classified as an asset or a liability at its then current fair value. In this case, the instrument is remeasured at fair value subsequently with fair value changes recognized in earnings.

If a warrant previously classified as a liability or asset needs to be re-classified to equity, the instrument is recorded in entity’s equity at the fair value on the reclassification date with no subsequent revaluation. There is no limit on the number of times a warrant may be reclassified.

Next Steps

SPAC sponsors and their service providers may consider alternative warrant terms, which will require balancing commercial interests and costs associated with the respective accounting treatment. One of the options is to make little or no changes to existing terms and classify both public and private warrants as a liability. Alternatively, SPACs may consider changing warrant terms to be able to classify the warrants as equity.

In general, to classify public and private warrants as equity, terms of fundamental transaction need substantial modifications to address observations 1 – 3 above. If the terms are revised so that the cash settlement is contingent on acceptance of the tender offer by more than 50% of all issuer’s securities, thus constituting a change in control, the above revision resolves issue 3 indicated above. For those SPAC that only one class of voting common stock, the above observation is not an issue. In an effort to classify warrants as equity instruments, many SPACs did away with existing cash settlement terms triggered by the change of control transaction.

Other changes required for equity classification include aligning terms of private and public warrants and adjusting the warrant table. Changes required to the warrant table are as such that revised amounts of net issuable shares under different scenarios is consistent with the outputs of standard Black-Scholes valuation model. Some SPACs decided to remove the warrant table and related settlement terms altogether.

Another alternative would be to a) keep private and public warrants separate and distinct from each other with no possibility of changes to their respective terms; b) ensure that private warrants are not subject to settlement terms per the warrant table. In this case, if substantial modifications to terms of fundamental transaction are made, private warrants can be classified as equity instruments. Classification of public warrants will largely depend on the terms of the warrant table.

As noted above, sponsors will need to decide among different alternative terms. The decision will require balancing commercial interests of SPAC public investors, SPAC management and the sponsor.

Appendix A

Accounting for Equity-Linked Instruments

Appendix-A

Appendix B

Accounting for Freestanding Equity-Linked Instrument

Appendix-B

Appendix C

Terms of Fundamental Transaction and Accounting Considerations

| Standard Terms | Accounting Considerations |

|

In the event of fundamental transaction (merger, consolidation, sale of company’s assets), warrant holders may be entitled to the same consideration including cash, shares or any other assets received by existing shareholders assuming warrant holders exercised their warrant rights immediately before the transaction subject to the following conditions: Condition A: if stockholders can elect as to the type and amount of considerations due to them, then consideration due to warrant holders will be weighted average amount received by stockholders. Condition B: if as a result of the transaction a party including its affiliates own beneficially more than 50% of outstanding common stock of the successor, warrant holders are entitled to receive the highest amount of cash, equity or other assets it would be entitled to if it exercised its warrant rights immediately before the transaction. |

Because of the condition B, warrant holders appear to enjoy more favorable settlement terms than other stockholders do since all warrant holders would be entitled to cash (or other assets), while only certain holders of Company’s common stock would be entitled to cash or the same amount of cash (or other assets). The above provision is not consistent with GAAP requirement that warrants holders would be entitled to the same consideration (e.g., cash, debt, stock) that all stockholders would be entitled to (ASC 815-40-55-2 through 55-5). Therefore, the warrants in question do not meet equity classification requirements. Terms of the above provision apply to both private and public warrants. Therefore, neither type of warrants meets equity classification requirement and should be classified as liabilities. |

|

If, in the event of fundamental transaction, the amount receivable by Company’s existing shareholders in shares of successor entity is less than 70% of the total consideration, warrant exercise price is adjusted to be the following amount: Per Share Consideration [A] – Black Sholes Warrant Value [B] [A] Per Share Consideration is the amount paid to existing holders of common stock as part of fundamental transaction. Additional terms apply to consideration paid in stock. [B] Black Scholes Warrant Value means Black Scholes value immediately before the fundamental transaction for a capped American call option according to Bloomberg financial markets. The value is determined considering warrant redemption terms. Terms of the warrant agreement specify how model inputs (risk-free rate, volatility and stock market price) are determined. Redemption/Transfer Terms: The Company has an option to redeem public warrants at $0.01 per warrant provided certain conditions are met. Conditions include trading price of common stock reaching certain level. Stock redemption is performed by issuing a 30-day redemption notice. Private warrants are not subject to redemption as long as they are held by the sponsors or permitted transferee, as defined in the warrant agreement. Private warrants cannot be transferred by sponsors until 30 days after completion of the business combination |

Private and public warrants have different redemption terms, which will impact their Black-Scholes value. As the holder of the instrument is not an input into the pricing of a fixed-for-fixed option on entity’s common stock, the warrants in question are not considered indexed to entity’s own stock (ASC 815-40-15-7E through 15-7H). The warrants do not meet equity classification requirements and should be classified as liability instruments. Liability instruments are measured at fair value initially and subsequently with changes in fair value reported in the income statement. Additionally, determination of whether the fundamental transaction took place and 50% beneficial ownership referred to in Condition B are determined based on Class A common shares only. Many SPACs have two classes of commons shares: Class A issued to public shares and Class B shares issued to sponsors. Class B shares typically make up 20% of SPAC’s shares following the IPO (exclusive of warrants). Change in control determined based Class A shares only may not constitute a change of control from the U.S. GAAP perspective, i.e. considering all voting shares. If there is no accounting change of control, cash settlement exception per ASC 815-40-55-2 through 55-5 does not apply. Therefore, the cash settlement provision is inconsistent with equity classification.

|

Important Note: FinAcco Consulting LLC is not responsible for, and no person should rely upon, any advice or information presented on this website. Note that entity’s financial statements, including, without limit, the use of generally accepted accounting principles (“GAAP”) to record the effects of any proposed transaction, are the responsibility of management. Therefore, any written comments by FinAcco Consulting LLC about the accounting treatment of selected balances or transactions or the use of GAAP are to serve only as general guidance. Our comments are based on our preliminary understanding of the relevant facts and circumstances and on current authoritative literature. Therefore, our comments are subject to change. FinAcco Consulting LLC does not assume any responsibility for timely updates of its website overall or any information provided in the Insights section of the website, specifically.